TDS & TCS Rate Chart 2026-27-Section-Wise Complete List | Traces Code 1001 to 1092

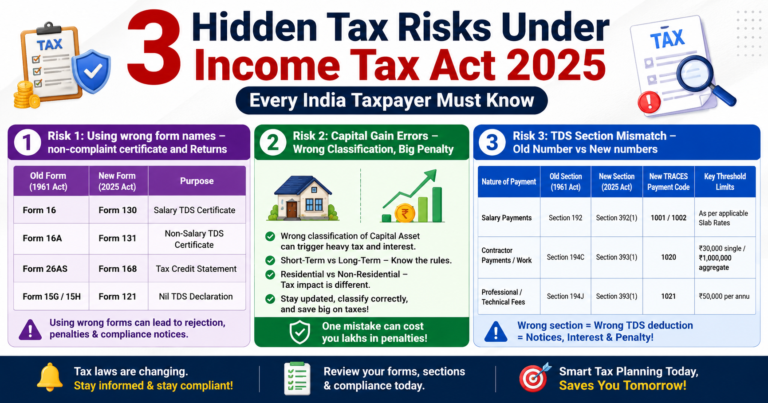

From 1 April 2026, the Income Tax Act, 2025 replaces the old Income Tax Act, 1961. All Traditional 194-series section-194C, 194J, 194H, 194A and others-stand abolished. Tax Year 2026-27 (FY 2026-27) operates under three new consolidated section.

Section 392 – Salary & EPF | Code 1001-1004 | Form 138

Section 393(1) – All non-salary resident payments | Code 1005-1038 | Form 140

Section 393(2) Non-resident / foreign payments | Codes 1039-1057 | Form 144

Section 393(3) Winnings, cash withdrawals, partner payments | codes 1058-1067

Section 394-TCS (Tax Collected at Source) | codes 1068-1092 | Form 143

Traces now requires 4-digit numeric payment codes (1001-1092) in all quarterly returns. Using old section numbers for Tax Year 2026-27 transactions causes portal validation errors. Finance Act 2026 also revises TCS rates on alcohol, scrap, minerals, tendu leaves, LRS remittance, and overseas tour packages.

Dull section-wise payment list with rates and thresholds is given below.

TDS Rate Chart FY 2026-27 PDF Download-Important Highlights & Full Free Download

Download TDS Rate Chart FY 2026-27 PDF – Traces code, old section mapping, rates and thresholds. Covers salary, rent, interest, contracts, property, VDA, non-resident and TCS in one printable PDF.

Download Important TDS Rate Chart PDF – FY 2026-27

TDS Rate Chart for FY 26-27 with new section and threshold limit

New TDS Section fy 26-27 pdf free download

Download Full TDS TCS Rate Chart-All 92 Codes

TDS / TCS Section-Wise Payment List-Tax Year 2026-27

Section 392 – Salary & EPF (Form 138, replaces Form

| Code | Old Section | Nature of Payment | New Section | Rate | Threshold |

| 1001 | 192 | Salary – State Govt /Local Authority employees | 392 | Slab | Basic exemption limit |

| 1002 | 192 | Salary – Union (Central) Govt employees | 392 | Slab | Basic exemption limit |

| 1003 | 192 | Salary – union (Central) Govt employees | 392 | Slab | Basic exemption limit |

| 1004 | 192A | Premature EPF withdrawal (before 5 yrs service) also Form 144 for NR employees | 392 (7) | 10% | ₹50,000 |

Section 393 (1) – Commission, Brokerage & Rent (Form 140)

| 1005 | 194D | Commission / brokerage – Insurance (by Insurance co.) | 393(1)[SI.1(i)] | 2% Indv 10% other | ₹20000 p.a. |

| 1006 | 194H | Commission / brokerage – all other (excl. BSNL/MTNL PCO) | 393(1)[SI.1(ii)] | 2% | 20000 p.a. |

| 1007* | 194IB | Rent by Individual/HUF not liable to tax audit (Inferred) | 393(1)[SI.2(i)] | 2% | 50000 / month |

| 1008 | 194I(a) | Rent-Plant. Machinery or Equipment (specified/audit-liable person | 393(1) [SL.2(ii).D(a)] | 2% | 50000 / month |

| 1009 | 194I(b) | Rent – Land, Building or Furniture (specified/audit-liable person | 393(1)[SI.2(ii).D(b)] | 10% | 50000 / month |

Immovable Property

| 1010* | 194IA | Purchase of Immovable property from resident (buyer deduct on higher of consideration of stamp duty value) (inferred) | 393(1)[SI.3(i)] | 1% | 50 lakh |

| 1011 | 164IC | Cash payment under Joint Development Agreement (Sec 67(14) | 393(1)[SI.3(ii)] | 10% | No threshold |

| 1012 | 194LA | Compensation on compulsory acquisition of immovable property | 393(1)[SI.3(iii)] | 10% | 5 lakh |

Dividend & Investment Income

| 1013 | 194K | Income from Mutual Fund / UTI specified company units | 393(1)[SI.4(i)] | 10% | 10000 p. a. |

| 1014 | 194LBA | Interest Income from Business trust (REIT/InvIT)- resident unit holder | 393(1)[SI.4(ii)] | 10% | No threshold |

| 1015 | 194LBA | Dividend-type income from Business trust-resident unit holder | 393(1)[SI.4(ii)] | 10% | No threshold |

| 1016 | 194LBA | Rental Income (REIT property) from Business Trust-resident unit holder | 393(1)[SI.4(ii)] | 10% | No threshold |

| 1017 | 194LBB | Income from AIF (Category I or II to resident unit holders | 393(1)[SI.4(iii)] | 10% | No threshold |

| 1018 | 194LBC | Income from securitization trust to resident investors | 393(1)[SI.4(iv) | 10% | No threshold |

| 1029 | 194 | Dividends by domestic company (including preference shares) | 393(1)[SI.7] | 10% | 100000 |

Interest on Securities & Deposits (Form 140)

| 1019 | 193 | Interest on securities – debentures, listed bonds, Govt securities | 393(1)[SI.5(i)] | 10% | 10000 p.a. (5000 debentures) |

| 1020 | 194A | Interest (not securities) – Bank/Post Office/Co-op-Senior Citizen (60+) | 393(1)[SI.5(ii) .D(a)] | 10% | 100000 p.a. |

| 1021 | 142A | Interest (not securities)- Bank/Post Office/Co-op-Other (<60yrs>) | 393(1)[SI.5(ii).D(b)] | 10% | 50000 p.a. |

| 1022 | 194A | Interest (not securities)- all other payers (companies, NBFCs, individuals | 393(1)[SI.5(iii)] | 10% | 10000 p.a. |

Contracts, Work & Professional Fees (Form 140)

| 1023 | 194C | Contracts payment-any sum for carrying out work (Individual/HUF) | 393(1)[SI.6(i).D(a)] | 1% | 30000 single / 100000 aggregate p. a. |

| 1024 | 194C | Contracts payment-any sum for carrying out work (individual/HUF) | 393(1)[SI.6(i).D(b)] | 2% | 30000 single / 100000 aggregate p. a |

| 1025* | 194M | Contract / commission / professional fees-Individual / HUF not liable to tax audit (where 194c/H/J not applicable | 393(1)[SI.6(ii)] | 2% | 50 lakh p.a |

| 1026 | 194J(a) | Professional fees-technical services, royalty for sale/distribution/exhibition of film | 393(1)[SI.6(iii).D(a)] | 2% | 50000 p.a. |

| 1027 | 194J(b) | Professional fees-all other professional / technical, services, royalty, non-compete fee | 393(1)[SI.6(iii).D(b)] | 10% | 50000 p.a. |

| 1028 | 194(b) | Remuneration/fees/commission to Director of company (non-salary) | 393(1)[SI.6(iii).D(b)] | 10% | – |

| 1032 | 194P | Payment to Specified Senior Citizen- Bank deducts TDS | 393(1)[SI.8(iii)] | Slab |

Goods, Perquisites, VDA & E-Commerce-Section 393(1) [SI.No.8]

| 1030 | 194DA | LIFE Insurance Police sum (taxable portion) Including bonus | 393(1)[SI.8(i)] | 2% | 100000 p.a. |

| 1031 | 194Q | Purchase of goods-buyer having turnover>10Cr | 393(1)[SI.8(ii)] | 0.1% | Excess of 50 lakh |

| 1033 | 194R | Business/Profession benefit or perquisite – in cash | 393(1)[SI.8(iv)] | 10% | 20000 |

| 1034 | 194R | Business/Profession benefit or perquisite – in kind/party in cash | 393(1)[SI.8(iv) note 6]] | 10% | 20000 |

| 1035 | 194O | E-Commerce: sale of goods/services by participant through operator | 393(1)[SI.8(v)] | 0.1% | 500000 (Indv./HUF) |

| 1036* | 194S | Consideration for VDA (crypto/NFT)-payer is Individual / HUF (non-audit category) | 393(1){SI.8(v)] | 1% | 50000 (specified person); 10000 (other) |

| 1037 | 194S | VDA Transfer – by persons other than Individual or HUF | 393(1)[SI.8(vi)] | 1% | 10000 |

| 1038 | 194SP | VDA Transfer-consideration I cash/kind/partly in cash and kind | 393(1)[SI.8(vi) Note 6] | 1% | 10000 |

Section 393(2)-Payment to Non-residents (Form 144, replaces form 27Q)

| 1039 | 195 | Other sums payable to non-resident (general NRI payments not covered by specific code) | 393(2)[SI.1] | As applicable | DTAA benefit may apply |

| 1040 | 194LC | Interest payable to NRI on bonds / Govt securities (1 Jul 2012 to 30 Jun 2023) | 393(2)[SI.2] | 5% | Plus surcharge + cess |

| 1041 | 194LC | Interest: Rupee Denominated bond borrowed outside India before 1 Jul 2023 | 393(2)[SI.3] | 5% | Plus surcharge + cess |

| 1042 | 194LC | Interest: LT bond/Rupee bond Listed on IFSC- Issue 1 Apr 2020-30 Jul 2023 | 393(2)[SI.4E(a)] | 4% | |

| 1043 | 194LC | Interest: LT bond/Rupee listed on IFSC-issued on/after 1 July 2023 | 393(2)[SI.4E(b)] | 9% | |

| 1044 | 19LB | Interest from Infrastructure Debt Fund to non-resident or foreign company | 393(2)[SI.5] | 5% | |

| 1045 | 194LBA | Business Trust: distributed income [Such’V SI.3.B(a) to NR unit holder | 393(2)[SI.6E(a)] | 5% | |

| 1046 | 194LBA | Business Trust: distributed income [Such’V SI.3.B(b) to NR unit holder | 393(2)[SI.6E(b)] | 5%/10% (Interest / Dividend) | |

| 1047 | 194LBA | Business Trust: distributed income [Such’V SI.4.B(b) to NR unit holder | 393(2)[SI.7] | 30% | |

| 1048 | 194LBB | AIF (Sec 224) income to nonresident unit holder-mom-exempt portion | 393(2)[SI.8] | 10% / 30% | |

| 1049 | 194LBC | Securitisation Trust (Sec 221) Income to non-resident investor | 393(2)[SI.9] | 30% | |

| 1050 | 196A | Income from units of specified Mutual Fund / specified company – non- resident | 393(2)[SI.10] | 20% | |

| 1051 | 196C | Income from units of offshore Fund (Sec 208) | 393(2)[SI.11] | 10% | |

| 1052 | 196B | LTCG on Transfer of Offshore Fund units (Sec 208) | 393(2)[SI.12] | 12.5% | |

| 1053 | 196C | Interest or Dividends on bonds / Global depository Receipts (Sec 209) | 393(2)[SI.13] | 10% | |

| 1054 | 196C | LTCG on transfer of bonds or GDRs (Sec 209) – non-resident | 393(2)[SI.14] | 12.5% | |

| 1055 | 196D | Income from securities (Sec 210(1))- Foreign Institutional investor | 393(2)[SI.15] | 20% | |

| 1056 | 196D | Income from securities (Sec 210(1))- Specified Fund [Sch.VI Note 1(g)] | 393(2)[SI.16] | 10% | |

| 1057 | 195 | Any interest/other sum chargeable-not salary-to NR or foreign company | 393(2)[SI.17] | Act/DTAA |

Winnings, Cash Withdrawals & Partner Payments Section 393(3) Form 140/144

| 1058 | 194B | Winnings from lottery / crossword / card game / gambling / betting – cash payment | 393(3)[SI.1] | 30% | 100000 per transaction |

| 1059 | 194B | Winning from lottery/gambling – paid in kind; organizer deposits tax before releasing prize | 393(3)[SI.1 Note 2] | 30% | 100000 per transaction |

| 1060 | 194BA | Winnings from online games – net winnings at year-end in user account- cash payment | 393(3)[SI.2 Note 2] | 30% | Full net winnings (no threshold) |

| 1061 | 194BA | Online game winnings-paid in king or partial cash; platform deposits tax before releasing | 393(3)[SI.2 Note 2] | 30% | 100000 per transaction |

| 1062 | 194BB | Winning from horse race | 393(3)[Si.3] | 30% | 100000 per transaction |

| 1063 | 194G | Commission / remuneration / prize on lottery tickets – to stockiest, distributor or ticker seller | 393(3)[SI.4] | 2% | 20000 p.a. |

| 1064 | 194N | Cash withdrawal from bank / PO co-op society – dedicatee is a co-cooperative society | 393(3)[SI.5D(b)] | 2% | 3 crore |

| 1065 | 194N | Cash withdrawal from bank / PO co-op society – dedicatee is any person other than a co-cooperative society | 393(3)[SI.5.D(b)] | 2% | 1 crore |

| 1066 | 194EE | Payment from National saving scheme (NSS)-withdrawal under section 80CCA(2)(a) | 393(3)[SI.6] | 10% | 2500 |

| 1067 | 194T | Salary / remuneration / commission / bonus / interest paid to partner of firm or LLP (incl. interest on capital account) | 393(3)[SI.7] | 10% | 20000 p.a. |

TCS – Tax Collected AT SOURCE

Traditional Goods – Section 393 Form 143

| Code | Old Section | Nature of Payment | New Section | Rate | Threshold |

| 1068 | 206C(1) | Sale of Alcoholic Liquor for human consumption | 394(1)[SI.1] | 2% | On every sale |

| 1069 | 206C(1) | Sale of Tendu Leaves | 394(1)[SI.2] | 2% | On every sale |

| 1070 | 206C(1) | Sale of Timber-obtained under a forest lease | 394(1)[SI.3] | 2% | On every sale |

| 1071 | 206C(1) | Sale of Timber-obtained under a forest lease | 394(1)[SI.3] | 2% | On every sale |

| 1072 | 206C(1) | Sale of other Forest Produce (not timber or tendu)-under a forest lease | 394(1)[SI.3] | 2% | On every sale |

| 1073 | 206C(1) | Sale of Scrap | 394(1)[SI.4] | 2% | On every sale |

| 1074 | 206C(1) | Sale of Minerals-coal, lignite, or Iron ore | 394(1)[SI.5] | 2% | On every sale |

| 1075 | 206C(1) | Sale of Motor Vehicle consideration exceeds prescribed limit | 394(1)[SI.6.D(a)] | 1% | 10 lakh per vehicle |

| 1076 | – | Sale of Wrist Watch (luxury) | 394(1)[SI.6.D(b)] | 1% | – |

| 1077 | Sale of Piece – antiques, plantings, sculptures | 394(1)[SI.6.D(b)] | 1% | ||

| 1078 | Sale of Collectibles-coins, stamps | 394(1)[SI.6.D(b)] | 1% | ||

| 1079 | Sale of Yacht, Rowing Boat, Canoe or Helicopter | 394(1)[SI.6.D(b)] | 1% | ||

| 1080 | Sale of pair of Sunglasses | 394(1)[SI.6.D(b)] | 1% | ||

| 1081 | Sale of Bag-handbag, purse (luxury) | 394(1)[SI.6.D(b)] | 1% | ||

| 1082 | Sale of pair of Shoes (luxury) | 394(1)[SI.6.D(b)] | 1% | ||

| 1083 | Sale of Sportswear and Equipment-golf kits, ski-wear etc. | 394(1)[SI.6.D(b)] | 1% | ||

| 1084 | Sale of Home Theatre System (luxury) | 394(1)[SI.6.D(b)] | 1% | ||

| 1085 | Sale of Horse for horse racing in race clubs or polo horse | 394(1)[SI.6.D(b)] | 1% | ||

| 1086 | 206C(1G) | LRS Remittance-for education or medical treatment (abroad) | 394(1)[SI.7.D(a)] | 2% | 10 lakh p.a. |

| 1087 | 206C(1G) | LRS Remittance-for any purpose other than education/medical | 394(1)[SI.7.D(b)] | 20% | 10 lakh p.a. |

| 1088 | 206C(1G) | Sale Overseas Tour Package-flat rate no threshold | 394(1)[SI.8] | 2% | |

| 1089 | 206C(1G) | 194(1) | 2% | ||

| 1090 | 206C(1C) | Grant of lease/licence for use of Parking Lot-for Business purposes (excl. Govt.) | 394(1)[SI.9] | 2% | |

| 1091 | 206C(1C) | Grant of lease/licence for Toll Plaza (excl. Govt.) | 394(1)[SI.9] | 2% | |

| 1092 | 206C(1C) | Grant of lease/licence for Mining or Quarrying-other | 394(1)[SI.9] | 2% |

TDS TCS Compliance Checklist – Tax year 2026-27 | What You Must Update Now

The section-wise table above covers all 92 TDS/TCS payment codes for Tax Year 2026-27 (FY 2026-27) under the Income Tax Act, 2025. Key compliance actions every deductor must complete:

Software & Returns Update Tally, SAP, or Zoho to use Traces codes 1001-1092. Old section numbers trigger validation errors. Replace Forms 24Q/26Q/27Q/27EQ|26QB, 26QC, 26QD with new forms 138|140|144|143|141.

Certificates & Declarations Issue Form 130 (replaces Form 16), for salaried employees. Accept Form 121 (replaces Form 15G|15H) for nil-TDS declarations and Certificates non-salary Form 131 (replace form 16A).

Rate changes (Finance Act 2026) TCS on alcohol, scrap, minerals raised to 2%. Tendu leaves reduced to 2%. Overseas tour packages now a flat 2% – no threshold, no two-tier slab. LRS education/medical reduced to 2% amounts above 10 lakhs.

Disclaimer: This TDS/TCS rate chart is for informational purposes only and does not constitute professional tax advice. Rates and Traces codes may change via CBDT notifications. Codes 1007, 1010, 1025, 1036 are yet officially notified. Always consult a qualified CA before filling returns.