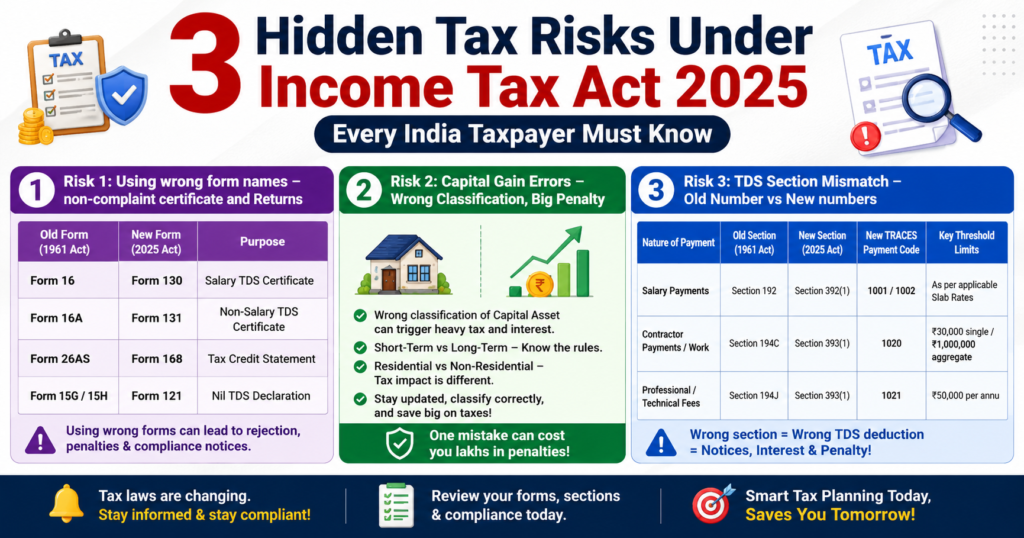

3 Hidden Tax Risks Under Income Tax Act 2025 Every India Taxpayer Must Know

India’s Income Tax Act 2025 officially replaced the old Income Tax Act, 1961 from 1 April 2026. For most taxpayers, this sounds like just a name change. But the reality is very different. The new law brings completely new section numbers, new from names, new challan codes, and a new reporting structure-and if you are not careful, event small mistakes can lead to tax notices, penalties, or rejection of your ITR.

Here are 3 real risks that every salaried person, business owner, and finance professional must be aware of under the new Income Tax Act 2025.

Risk 1: Using Wrong Form Names – Non-Complaint Certificate and Returns

This is the most overlooked risk – and it affects both employers and employees directly.

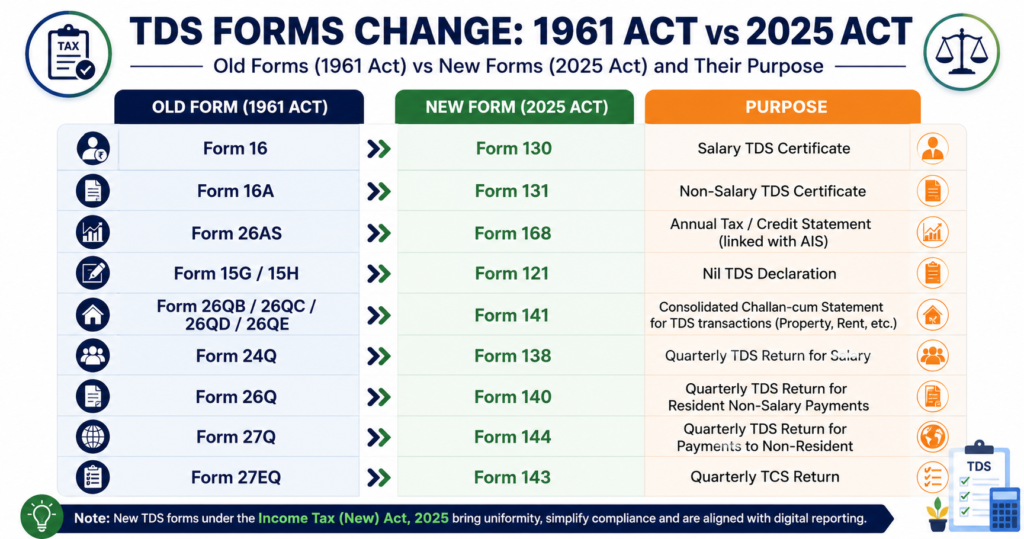

Under the Income Tax Act 2025, almost every major TDS form has been renamed:

| Old Form (1961 Act) | New form (2025 Act) | Purpose |

| Form 16 | from 130 | Salary TDS Certificate |

| Form 16A | from 131 | Non-Salary TDS Certificate |

| Form 26AS | from 168 | Annual Tax /Credit Statement (linked with AIS) |

| From 15G/15H | form 121 | Nail TDS Declaration |

| Form 26QB/26QC/26QD/26QE | form 141 | Consolidated challan-cum Statment for TDS transaction (property, rent, etc.) |

| Form 24Q | form 138 | Quarterly TDS Return for Salary |

| Form 26Q | form 140 | Quarterly TDS Return for Resident Non-Salary Payments |

| Form 27Q | form 144 | Quarterly TDS Return for Payments to Non-Resident |

| From 27EQ | Form 143 | Quarterly TCS Return |

If your employee issue you Form 16 for tax Year 2026-27 salary, that document is technically non-compliant. The correct form is now Form 130. If you try to use from 16 for ITR filing. The e-filing portal may show a mismatch – because the portal will be looking for Form 130 data.

Similarly, if vendor submit the old Form 15G or 15H for nil TDS declaration, it will not be valid for Tax Year 2026-27. They must now use from 121.

What to do: Ask your employer, bank or payer to issue the correct new forms. If they are not aware, share this information with them proactively.

Risk 2: Capital Gains Errors – Wrong Classification, Big Penalty

Capital gains is one area where even educated taxpayers make mistakes – and the Income Tax Act 2025 has not made it easier.

The most common error is misclassifying Long-Term Capital Gains (LTCG) as Short-Term Capital Gains (STCG), or vice versa. The holding period is the factor here:

Equity shares or mutual funds held for more than 12 months = LTCG

Property held for more than 24 months = LTCG

If you sell shares and your broker reports the transaction in AIS (Annual Information Statement) but you report it under the wrong category in your ITR, the Income Tax Department system will flag a mismatch.

Tax experts point out that in capital gains reporting, missing details like holding. periods or corporate actions (like bonus share, stock splits) often lead to wrong classification event a small difference between LTCG and STCG treatment can significantly change your final tax liability.

What happens if wrong classification? Under Section 270A of the new Act misreporting income can attract a penalty of up to 200% of the tax due. This is not a small amount-it can be financial devastating.

What to do: Cross-check every capital gains transaction against your IAS/form 168 data. If you have received bonus shares or participated in buybacks, consult a CA before filing.

Risk 3: TDS Section Mismatch – Old Number Vs New numbers

This is the biggest risk right now, especially for employers, accountants, and deductors.

Under the old Income Tax Act 1961, TDS sections had familiar names – Section 194C for contractors, Section 194J for professionals, Section 194I for rent, and so on. But under the new Income Tax 2025, all these separate sections have been merged into Section 393 (for non-salary payments) and Section 392 (for salary TDS).

If your companies TDS software, ERP system, or payroll tool has not been updated, it may still be filing TDS returns using old sections number like 194C or 194J for transactions happening after 1 April 2026. This creates a mismatch in the system.

The Income Tax Department has already warned that during the transaction, period, mismatches may arise if deductors quote old section number for post April 2026 transactions, or if the wrong assessment year (AY) if selected on the challan. The new challan is called ITNS 281N and the payment Codes are now numeric – ranging from 1001 to 1067 – instead of section Names.

What happens if mismatch occurs? Your TDS credit may not reflect correctly in the deductee’s form 168 (the new Form 26 equivalent). This means the employee vendor claim their TDS credit while filing their return-leading to higher tax liability, refund delays, or demand notices.

Final Takeaway

The Income Tax Act 2025 is not just a rewrite- it is a full restructuring of Indian tax complaint system. The core tax rates have not changed much, but the way your report, file and certify has changed completely.

Whether you are salaried employee, a business owner, or a finance professional, the biggest risk right now is assuming that nothing has changed. Update your knowledge, update your software, and verify your forms-because under the new Act, procedural errors are treated as seriously as tax evasions.